The Case on Reddit (RDDT)

This analysis was built with Secaura, institutional-grade equity research, accessible. Every figure below is pulled directly from SEC filings.

Reddit went public in March 2024 as a beloved, butunprofitable internet forum that had never figured out how to make money off the eighteen years of human conversation sitting on its servers. Two years later, the narrative has flipped that the stock now trades like an advertising platform with an AI-data call option stapled to the side. The Q1 2026 10-Q, filed May 1, 2026, is the document where that transformation stops being a story and becomes arithmetic.

This report works through that arithmetic in full. The headline is genuinely impressive, revenue up 69% year-over-year, a 27.6% operating margin, and diluted EPS of $1.01 against $0.13 a year ago, but the interesting questions live underneath it. Why did margins inflect? Is the growth coming from more users or more money per user? How fragile is a business that depends on Google for its front door? And is the AI-licensing thesis everyone is paying for actually visible in the numbers yet?

The short version: this is a monetization story, not a user growth story, and certainly not yet an AI story. The bull and bear cases are both real, and the entire debate collapses into a single question about valuation. Let’s build to it.

1. Profitability inflected — but read the operating line, not the EPS

Here is the Q1 2026 income statement against Q1 2025, taken verbatim from the filing:

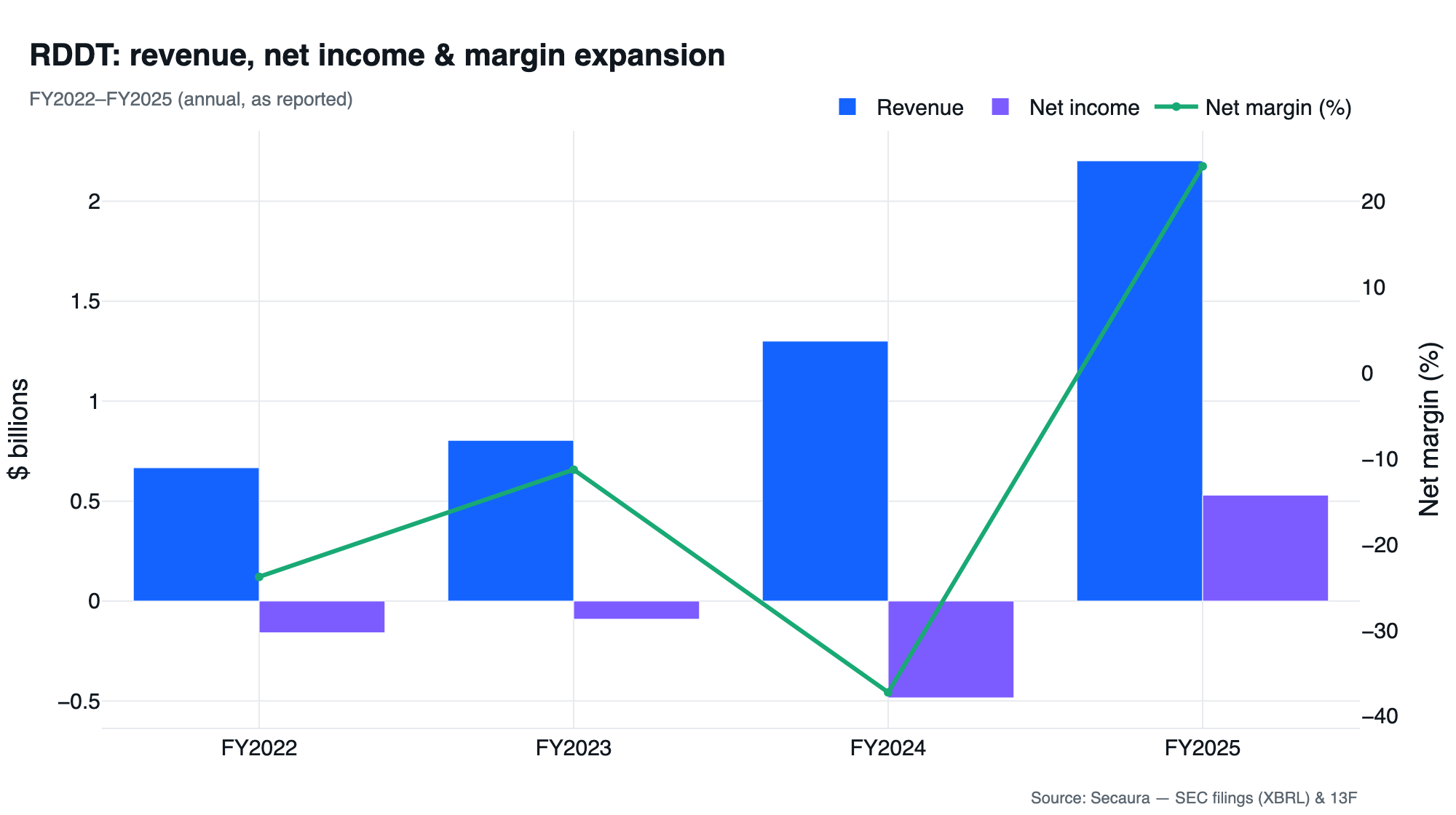

The multi-year arc on the chart above tells the real story. Reddit lost $158.6M in FY2022, $90.8M in FY2023, and $484.3M in FY2024 (the last figure inflated by IPO-related stock based compensation), then swung to $529.7M of net income in FY2025. The Q1 2026 print isn’t a one-quarter fluke; it’s the continuation of a margin curve that turned the corner sometime in 2025.

But a careful analyst separates operating profitability from reported profitability, and Reddit is a textbook case for why that distinction matters. Net income of $203,981K is actually $21,069K larger than operating income of $182,912K. Two below the line items explain the gap:

Other income of $22,816K, which the MD&A defines plainly:

“Other income (expense), net, consists primarily of interest income, interest expense, realized gains and losses on sales of marketable securities, and foreign currency transaction gains and losses.”

This is the yield on Reddit’s $2.77 billion of post-IPO cash and marketable securities . Real, but it is treasury income, not the operating business, and it will fall if rates fall.

An almost-zero tax bill of $1,747K, a 0.85% effective rate. The filing is explicit about why: Reddit carries a full valuation allowance against its U.S. deferred tax assets, so its accumulated losses are currently shielding nearly all of its income from tax. The 10-Q then drops the single most important forward-looking sentence in the document:

“Given our recent history of generating net income in the United States, we believe that there is a reasonable possibility that sufficient positive evidence may become available within the next 12 months to allow us to release a significant portion of the valuation allowance... The reversal would result in a significant income tax benefit in the period when we release it.”

For a value investor this is a double-edged disclosure. In the near term, releasing the valuation allowance produces a one-time, non-cash income-tax benefit that will make some future quarter’s EPS look enormous, and it will be low-quality, a paper gain. After that, Reddit’s go-forward tax rate normalizes toward a real corporate rate, which means today’s $1.01 EPS overstates the company’s steady-state earnings power. The cleaner, more durable read on profitability is the 27.57% operating margin, and that number is excellent on its own merits.

One more quality-of-earnings point in Reddit’s favor: this is an asset-light model. Capital expenditures were just $1,090K on $663M of revenue (0.16%) because Reddit rents its infrastructure rather than building data centers. The result is that free cash flow (FCF) of $311.2M actually exceeded net income (vs. $126.6M a year ago), and gross margin ticked up to 91.5% from 90.5%. When FCF runs ahead of reported earnings, the earnings are generally conservative, not aggressive. That is a meaningful offset to the tax-rate caveat above.

2. The real engine is monetization, not users

The instinct with a 69% revenue grower is to assume the user base is exploding. It isn’t. Daily Active Uniques (DAUq) were 126.8 million, up only 17% year-over-year, and that growth rate is decelerating with metronomic consistency. The MD&A’s own eight-quarter table:

Total DAUq YoY Growth: 51% → 47% → 39% → 31% → 21% → 19% → 19% → 17%

The logged-in cohort, historically Reddit’s higher-value users, is decelerating even faster: 31% → 27% → 27% → 23% → 17% → 14% → 10% → 7%. (Note a transparency wrinkle: management states that “beginning in the quarter ended September 30, 2026, we will no longer report logged-in and logged-out DAUq,” which removes investors’ clearest window into engagement quality.)

So if users grew 17% and revenue grew 69%, the difference is money extracted per user. That is exactly what happened: Average Revenue Per User (ARPU) reached $5.23, up 44% year-over-year from $3.63. This is the single most important operating metric in the filing, because ARPU expansion is far more valuable than user growth, it requires no incremental user acquisition cost and drops almost entirely to the gross-margin line on a 91.5%-margin business.

What’s driving ARPU is itself worth decomposing, because the filing hands us the pieces. Advertising revenue (94% of the total) grew +74%, and the MD&A attributes it to two factors that both rose about 32%:

Ad impressions delivered increased by approximately 32%, and

The price of ads increased by approximately 32%.

Those compound: 1.32 × 1.32 ≈ 1.74, i.e. the +74% ad-revenue growth is roughly half volume and half price. The pricing half is the part that should excite investors. It signals genuine pricing power and advertiser demand, not just cramming more ads onto the page.

The geographic story frames the runway and its catch in the same breath. Rest-of-world DAUq grew 26% versus just 7% in the U.S., and rest-of-world weekly actives grew 33% versus 10% domestically. International is clearly where the user growth lives. But the monetization gap is stark: U.S. ARPU is $9.63 versus just $2.02 in the rest of the world, a 4.8x gap. So Reddit’s fastest-growing users are its least monetized, which means international expansion lifts the user count far more than it lifts revenue in the near term. The runway is real; it’s just a long, low-yield one.

3. The structural risk hiding in plain sight: Google

If there is one thing that should genuinely worry a Reddit shareholder, it is the company’s dependence on a single, conflicted counterparty. The Risk Factors are unusually blunt:

“Our success depends partly on our ability to attract online visitors to our website. We rely, in part, on internet search engines, such as Google, to generate traffic to our website, primarily through free or organic searches.”

“If a major search engine changes its algorithms in a manner that negatively affects the search engine ranking performance of our website... our business, results of operations, financial condition, and prospects could be adversely affected.”

This is not abstract. The MD&A explicitly credits Reddit’s Q1 DAUq growth in part to “third-party search engine algorithm changes“, meaning a non-trivial share of the good news this quarter was a gift from Google’s ranking decisions, decisions Reddit does not control and that can reverse without warning. And the company tells us these search-sourced users are precisely the low-value cohort:

“Visitors that come to Reddit from search engines are generally not logged in... Currently, monetization of these users is mainly through conversation pages and feed ads.”

So the fast-growing, Google-fed traffic is also the lowest-monetizing traffic, and it sits at the mercy of an algorithm owned by a company that is, simultaneously, Reddit’s largest traffic source, a cloud vendor, a data-licensing customer, and through AI Overviews, a direct substitution threat. The filing names that last danger specifically:

“Redditors may choose to find information using AI tools, which in some cases may have been trained using Reddit content, instead of visiting Reddit directly.”

Read that twice. The same corpus Reddit is licensing to AI companies could be used to build the products that make visiting Reddit unnecessary. This is the deepest tension in the entire investment case: Reddit’s content is valuable because it is the human substrate the AI era is built on, but that same dynamic could disintermediate Reddit’s own traffic funnel.

Quantifying the bear case: Roughly 94% of revenue ($624,670K of $663,411K) is advertising, and that advertising is volume-times-price on a traffic base that is materially search-dependent. A useful stress test: if a Google algorithm change or AI-Overview cannibalization knocked logged-out traffic enough to take total revenue down 10% from the Q1 run-rate, you would lose roughly $66M of quarterly revenue at ~91% incremental margin, call it ~$60M of operating income, which would cut the 27.6% operating margin to roughly 20% and compress EPS far more than 10% because of operating deleverage. The point isn’t that this will happen; it’s that the revenue base is more concentrated and more externally dependent than the clean growth numbers suggest, so it deserves a higher discount rate than a diversified ad platform like Meta.

4. The AI-licensing option: real, scarce, and still tiny

Now the part of the story doing the most work in investors’ imaginations and the least work in the income statement. Reddit owns one of the largest corpora of authentic, structured, human conversation on the internet. Exactly the training data large language models are starved for. The thesis writes itself. The numbers, less so.

Content licensing lives inside the “Other revenue” line, which was $38,741K in Q1 2026, up just 15% year-over-year (from $33,731K), versus advertising’s +74%. In other words, the AI-data business is roughly 6% of revenue and is growing slower than the company as a whole, which means it is shrinking as a share of the mix, not expanding. That is the opposite of what the “Reddit is an AI-data play” narrative implies.

The contracted backlog confirms it’s early and front-loaded rather than a durable annuity. From the revenue note:

“As of March 31, 2026, the aggregate amount of remaining performance obligations in contracts with an original expected duration exceeding one year was $120.6 million... We expect to recognize $91.6 million in the remainder of 2026 and $29.0 million in 2027.”

So three-quarters of the contracted licensing backlog burns off within nine months, and only $29.0M is committed to 2027. This is not yet a recurring, multi-year revenue stream, it’s a handful of large deals running off. Management does not oversell it:

“We are in the early stages of our content licensing efforts, and the market for content is new and evolving rapidly. There is no assurance that we will be able to sustain revenues from these efforts.”

The genuinely intriguing kicker is enforcement. Reddit is not merely waiting for buyers; it is going after non-payers:

“Some companies have constructed very large commercial language models using Reddit content without entering into a license agreement with us. While we have commenced litigation and will continue to vigorously enforce against such entities, such enforcement activities could take years to resolve, result in substantial expense... and we may not ultimately be successful.”

There is also regulatory friction, the Dutch data-protection authority “has inquired into and ordered access to information about our content licensing efforts, which we are contesting.” The honest characterization of AI licensing today: high-value, scarce, defensible data, but an unproven, lumpy, and contested revenue line that is a medium-risk optionality kicker, not a reason to own the stock at today’s price. If you are paying for Reddit because of AI licensing, you are paying for something that is currently 6% of revenue and decelerating.

5. Where the big money actually moved

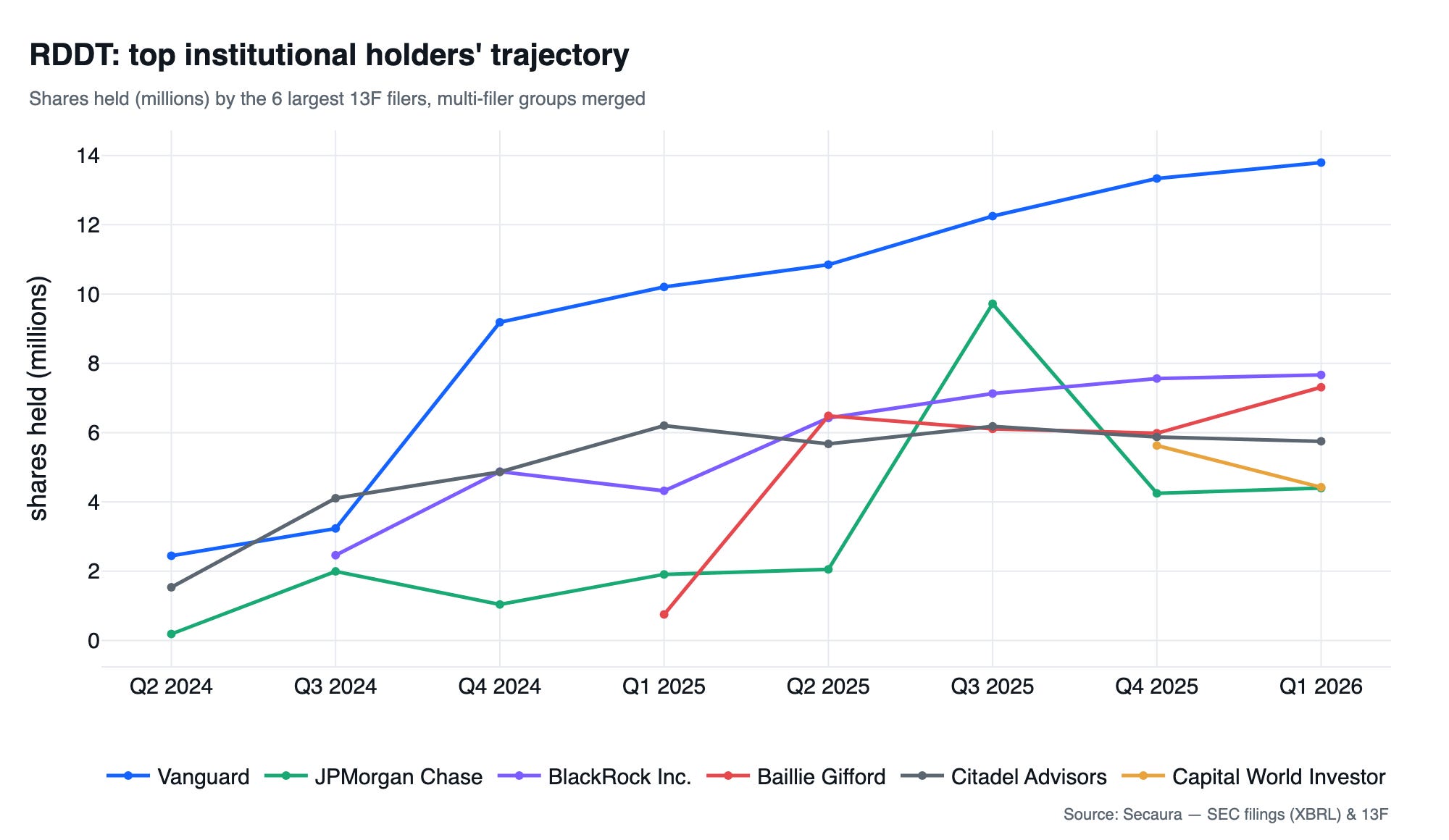

Institutional 13F filings, positions as of March 31, 2026, show this is decidedly not a one-way tape. The split between patient index/growth capital and twitchy active funds is the most informative pattern in the ownership data.

Accumulating:

Vanguard has added in every single quarter since Reddit’s 2024 IPO, eight straight taking its combined position from 1.67M shares (Q1 2024, the IPO quarter) to 13.79M (Q1 2026), now the single largest holder we track.

BlackRock grew from 4.87M (Q4 2024) to 7.66M (Q1 2026), roughly +57%.

Baillie Gifford, a long-horizon growth shop, built a position essentially from scratch, 0.75M in Q1 2025 to 7.31M by Q1 2026, exactly the kind of decade-holding capital you want as a long-term shareholder.

Distributing:

Fidelity (FMR), once the largest holder at a 13.49M-share peak (Q3 2025), slashed it to 2.92M, down ~78% in two quarters. (Note: Fidelity led the series F funding round in 2021, so I think it’s only natural they cut down on their positions)

Coatue more than halved, from a 6.53M peak to 2.79M. (Note: Coatue participated in the series C funding round in 2017)

D.E. Shaw drifted lower (4.80M → 2.73M), and Capital World Investors trimmed ~21% in the latest quarter.

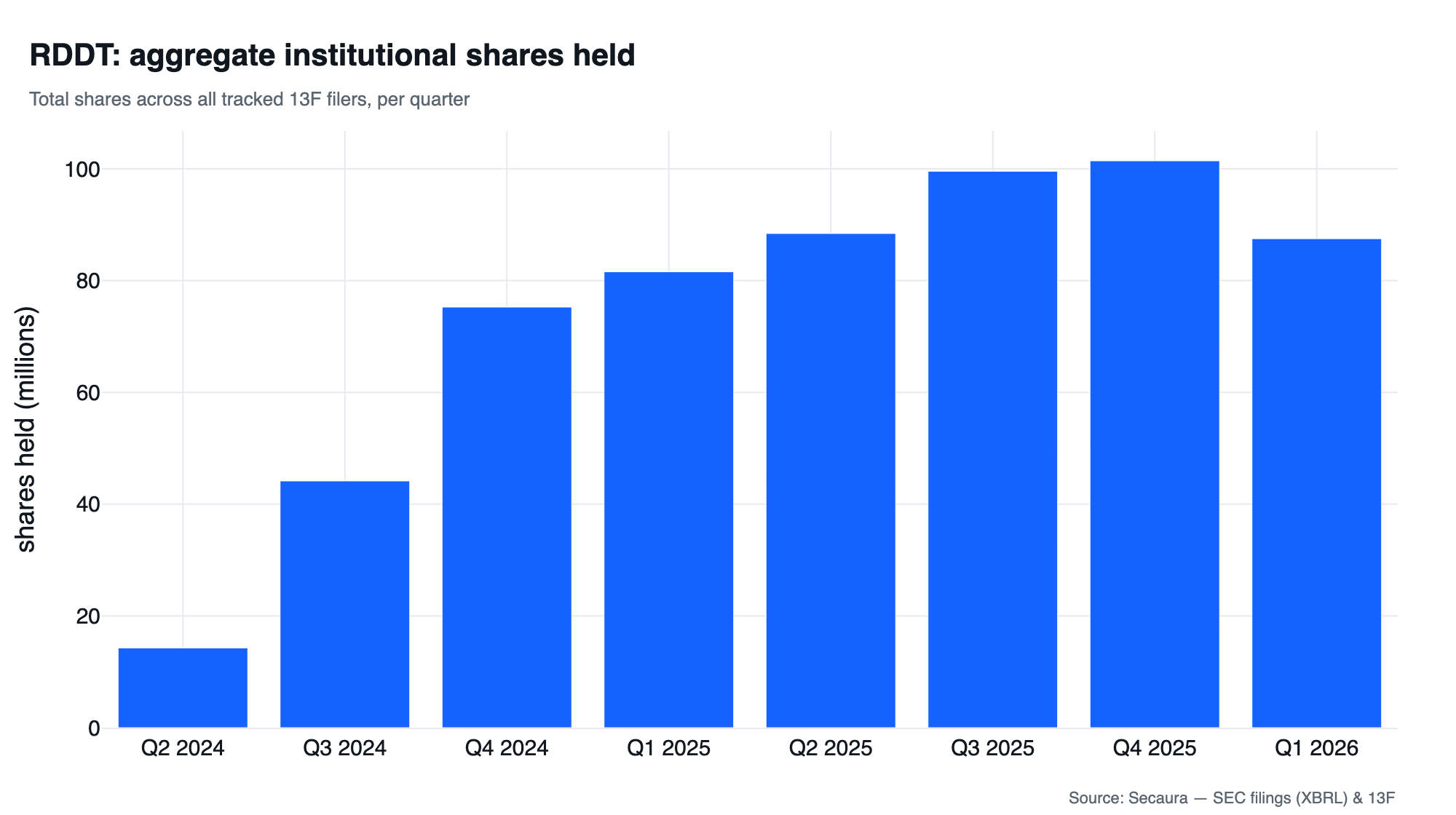

The aggregate picture (above) is telling. Total institutional shares held climbed steadily from 14.3M (Q2 2024) to a peak of 101.4M (Q4 2025), then dipped to 87.5M in Q1 2026, the first quarterly decline in the series. That dip is not passive money leaving; it is the active funds (Fidelity, Coatue, Capital World) heading for the exits faster than the index and growth shops added given the fact that some of them were investors prior-to-IPO. The signal to extract: the marginal long-term, valuation-insensitive buyer (Vanguard, BlackRock, Baillie Gifford) is still accumulating, while the marginal trade-the-momentum buyer is taking profits after a huge run. That is what distribution looks like in a stock that has tripled, informative about positioning, but not a verdict on the business.

The institutional ownership trajectory and valuation tools above are live on Secaura, explore any of ~100 companies’ 13F flows, filings, and fundamentals yourself.

(Standard 13F caveats apply: these filings capture only large institutional managers, reflect March 31 positions, and lag by up to 45 days, so this is the direction of the biggest owners, not a complete or fully current ownership picture.)

6. Valuation: the entire debate, in one section

Everything above resolves to a single question, is the growth durable enough to justify the multiple? Let’s set up the math cleanly.

The setup (June 18, 2026 close):

Price $174.96 × ~201.96M diluted shares = market cap ≈ $35.34B

Cash & equivalents $1,374.3M + marketable securities $1,396.3M = $2.77B, against essentially zero debt (Reddit’s revolving credit facility is undrawn).

Net cash ≈ $2.77B, or ~$13.72/share.

Enterprise value ≈ $32.57B

TTM (Q2 2025–Q1 2026): revenue $2,473,556K, net income $707,544K, diluted EPS $3.50

The trailing multiples:

P/E (TTM) ≈ 50.0x ($174.96 ÷ $3.50)

P/S (TTM) ≈ 14.3x ($35.34B ÷ $2.47B)

EV/Sales (TTM) ≈ 13.2x ($32.57B ÷ $2.47B)

A note on which multiple to trust: the P/E is the least reliable of the three, for the exact reasons in Section 1, net income is flattered by treasury interest income and an artificially low 0.85% tax rate that will normalize upward. The EV/Sales multiple of ~13x is the cleaner gauge of what the market is paying, and it strips out the $2.77B cash pile that the P/S includes. Either way, these are unambiguously growth-stock multiples.

Historical context. Is ~14x sales cheap or expensive against Reddit’s own short history? With only two years of public trading and a stock that has ranged from a $39.17 to $270.71 closing range all-time, the multiple band is wide and not yet a stable anchor.

What’s priced in (reverse logic). A ~13x EV/Sales multiple on a software-like, 91%-gross-margin, FCF-positive platform is not absurd if growth stays high. The way to sanity-check it: at this multiple the market is effectively underwriting something like 40%+ revenue CAGR for the next two-to-three years, decelerating gracefully thereafter, with the operating margin continuing to expand past 30%. If Reddit delivers that, the multiple compresses naturally as the denominator grows and the stock can work from here. If growth disappoints to, say, the 20s, today’s price has no margin of safety.

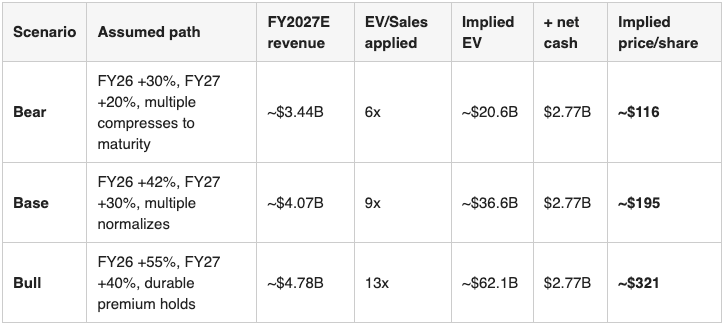

Scenario grid. Below, illustrative FY2027 revenue scenarios are paired with an EV/Sales multiple, then net cash is added back and the total divided by ~201.96M diluted shares. Every growth figure is a labeled assumption, not a forecast. This is scenario math, not a price target.

(FY2025 actual revenue was $2,202,506K; growth applied off that base. Implied price = (FY27E revenue × multiple + $2.77B net cash) ÷ 201.96M shares.)

The grid frames the asymmetry honestly. Today’s $174.96 sits below the base case (~$195) and well above the bear (~$116), so the market is currently pricing something between “base” and “bear,” demanding proof that the 40–50% growth is durable before it underwrites the bull outcome. A margin-of-safety-minded investor would note that the downside to the bear case (~−34%) is comparable in magnitude to the upside to the base case (~+11%), and the genuinely large returns require the bull path — i.e. you are not being paid a wide margin of safety to wait. The investment case lives entirely in the durability of ARPU-led growth.

7. The verdict

Strip away the AI narrative and you are left with something simpler and, frankly, better than the hype: a high-margin, asset-light advertising platform that has just proven real pricing power, expanding margins, and free cash flow that exceeds reported earnings. The monetization engine, ARPU +44%, driven by impressions and price each up ~32%, is the genuine story, and it is a good one.

The bear case is equally real and should not be hand-waved: user growth is decelerating every quarter, ~94% of revenue is one ad business, the traffic funnel is hostage to Google’s algorithm and to AI-Overview substitution, and the celebrated AI-licensing line is still 6% of revenue and shrinking as a share of the mix. The valuation prices in success, not failure, so the burden of proof sits with the bulls.

Our read: the investment case rests on continued ARPU expansion in the core advertising business, full stop. AI licensing is a real, scarce, defensible option, worth watching, occasionally worth a headline pop, but it is not yet a reason to own the stock, and pretending otherwise is how investors overpay. At ~13x EV/sales with the marginal active fund already selling, RDDT is a high-quality business at a price that requires the growth story to keep delivering for several more years. Whether you find that compelling depends entirely on how durable you believe 40%+ growth is on a 126-million-user base growing 17%.

Written using Secaura , institutional-grade equity research, accessible. Start exploring →

Disclaimer: This is an analysis of SEC filings for educational and discussion purposes only. This is not financial advice. Do your own due diligence (DD).